Consolidating The Lessons From The #AfricaSaves Challenge

3 months ago, we set out on a savings challenge, sponsored by Barclays. The aim of the challenge was not about saving a fixed amount of money (though we had a goal), but to train our brains to cope with delayed gratification. While we are good at setting goals, accomplishing them is difficult. This is because our hands always reach for what we want now, ignoring our hearts, which hold what we want to achieve long term.

To train our brains, we did a number of things:

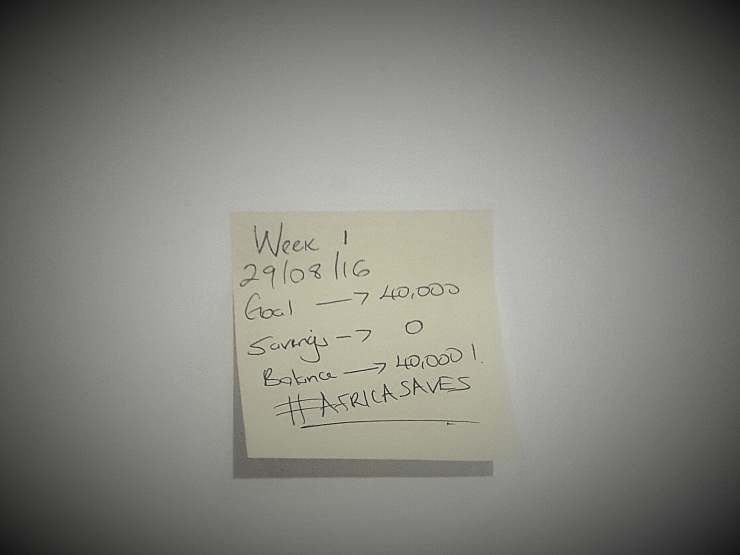

- We set a savings goal which is the first step in achieving anything, and is key to stay . My goal was to save 40,000 shillings towards a loan repayment.

- For a week, we tracked our spending, without changing our spending habits. The goal of this was to see which areas we impulse spent the most. By changing our habits, we could save money. The aim was to restrain the Hand that reaches out.

- We identified areas where we spent impulsively the most. Mine was breakfast and lunch at work. I spent between 1,500 – 4,000 per week on this. My goal was to organize myself enough, to carry food to work daily saving this money. By using the Barclays savings calculator we are able to see how much we save when we stop spending on those impulses.

- We identified things we needed to do to make it easy for us to implement habit changes. Setting up the right systems ensures that we are not derailed. For me, this meant meal planning, buying more lunch boxes and having some breakfast items at work for those days I did not pack my breakfast the night before.

- Sometimes we get derailed (like I did), but the most important thing is to recover and stay the course. Often we fail to achieve our goals because once we fail for a day/week/month, we give up and revert to our old habits.

- Finally, we learned how to review our goals and to give them a long-term view. Reviewing motivates us, because it enables us see how well we are doing, and to correct any deviations.

I found two things immensely useful throughout this challenge. First, the accountability aspect of it. Throughout the challenge, I had a sticky note right above my bed, reminding me every day that I had a goal, and the day’s actions would determine whether I would accomplish my goal or not. Also, the knowledge that I would be accountable to both the readers of this blog and on Twitter kept me focused.

Secondly, the constant reminder of the importance of consistency, and to keep my vices. Every so often while on YouTube, I would find myself re-watching the Barclays videos to keep the tips top of mind.

What did I achieve?

Last week, I sent 45,000 shillings to the bank, towards my loan repayment. What is remarkable is not the amount or the repayment, but the fact that this was from savings I otherwise would not have made. If I had not changed my habits, I would have needed to eat into my savings for this.

Thanks to a small tweak in my habits, I now have extra money I can spend as I please. At the last post, I committed to keep investing this money towards my daughter’s education fund.

As we approach the end of the year, what savings goals do you have? What do you intend to do in order to achieve those goals? Let us discuss in the comments section, and on Twitter using the #AfricaSaves hashtag.

This article is the final in a series of sponsored posts for the BARCLAYS SAVINGS CHALLENGE. I hope the challenge has been as interesting and impactful for you as it has been for me. You can follow the discussion on Twitter and Facebook and share your own experience by using the hashtag #AFRICASAVES. Visit the Barclays page for useful savings calculators and information on their savings accounts.