Fallacies and Exaggerated Benefits Of A Mortgage

This morning, the post below crossed my Twitter timeline…

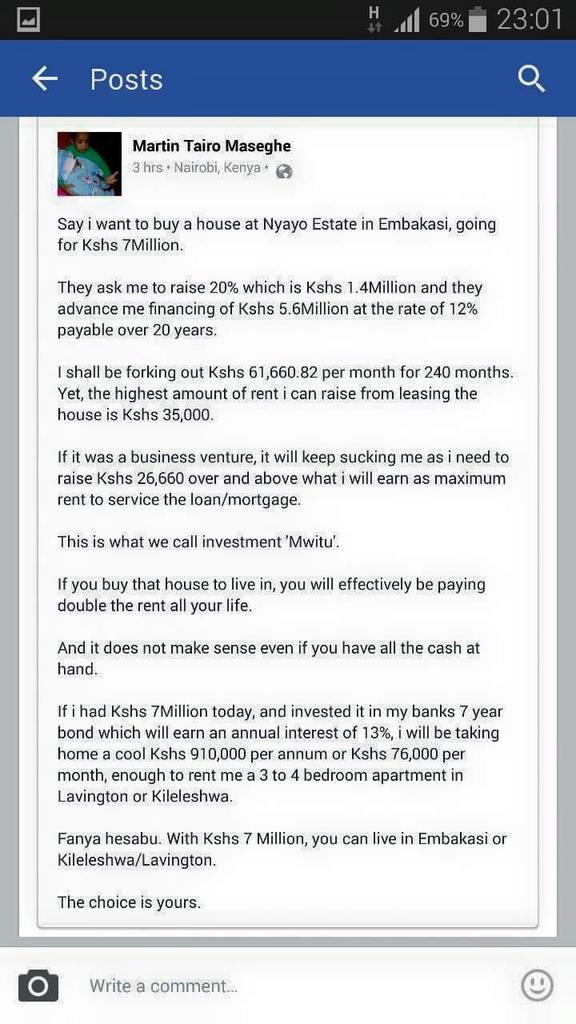

Click to enlarge

It spurred a discussion that seems to come up on my Twitter timeline every so often: home ownership and its advantages (and disadvantages). I have blogged extensively on the benefits of buying a house and mortgages, so for this post I would like to point out fallacies/untruths/exaggerations that are quoted as people explain the benefits of taking a mortgage.

1. The value of the house will double in xx years.

While it is true that real estate appreciates, it is fallacious to assume that house values will always appreciate, and to take it further to know that the value will definitely double. In the last 10 years, Nairobi has experienced crazy growth in real estate where house values have doubled and tripled in a short time, but like we say in finance “trees do not grow to the sky”. A short period of crazy growth is not indicative of the future. It is important to consider factors that are leading to this growth, and whether the growth is sustainable in the long term. If you are taking a 15 year mortgage, you need to consider what could change in 15 years and the effect of that change on the value of your home.

If we are talking about apartments, one needs to consider changes in city lifestyles and what they will mean for the value of your home. If a neighbourhood changes negatively, the value of your apartment will actually go down in the long term. If you have an old house and a developer builds swanky apartments next to your house, you are likely to lose value especially if you bought your apartment today, at an inflated price. Someone bought an apartment in old Madaraka 4 years ago for Kshs 5 million, and today she is getting offers for Kshs 5-5.5 million on the same apartment because new apartments came up right next.

Real estate does appreciate, but the doubling in xx years is at best speculation.

2. A mortgage is a fixed expense unlike paying rent

The above statement assumes that once you have taken a mortgage, that is it. The cost of your home is fixed for the next 15 years. While loan repayments are fixed, costs of home ownership are not fixed and they in fact increase as your house grows older. If you are buying a ready apartment/house, you have no guarantee on the quality of the fixtures, and once they break down, you do not have the option of moving to another home, or calling a landlord to fix it. A plumbing issue could easily cost you 10% of the value of your house to fix.

In addition to maintenance costs, you have to consider land rates which are due to the city council. If there are changes in the neighborhood requiring home owners to contribute (like building roads and services), you have to pay. If you have rented a house, those costs are borne by the owner.

The mortgage payment is fixed, the cost of a home is not fixed, neither is it predictable.

3. Unlike a mortgage, rent prices can be increased any time by the landlord and this cancels out any investment you may make with the funds you could invest in a house.

This is partly true. When you have rented a house, the landlord has the freedom to increase the rent anytime. What is fallacious about the above statement is that by choosing to rent and investing that money, your return is lost because your rent is growing. The consideration here should be: how much does rent increase in a space of 10-15 years? If you live in the same house for 10 years, your landlord is likely to revise your rental every 3-5 years, and not by more than 5% each time, while the bond investment quoted above grows by 13% every year.

While rentals do in fact increase, that increase isn’t significant. This should also be instructive of individuals buying houses to rent out. By how much will your rental income increase annually?