Looking to own a bank? A comparison of Equity and KCB banks’ stocks

The NSE has some 66 odd listed companies. Unless analyzing companies is your day job or someone else is paying for it, it is impractical to obtain and analyze usable information on every single one. My strategy as shared in an earlier post is to keep my radar up and when something comes up at a high-level, it registers on my radar screen for further analysis.

Such an event is the Interest Cap law imposed on banks in 2016. Its coming into force was an important enough event to send one’s attention to the financial counters. Similarly, its imminent repeal or modification must register, leading to some interest. My action after looking at the sector closer is to take a bullish (or optimistic) position on it. My stocks of choice are Equity Group Holdings and KCB Group. Two reasons for this: they register on my radar as the leaders in digital innovation for banking the masses, and their fundamentals are very attractive and can only get better with the interest rate cap regime gone.

I have a personal preference for Equity Group between the two. And I have a couple investor friends who do not quite feel the counter as I do. So as a way of introducing technical analysis my way – which I keep completely simple because those 30 page pieces that career analysts do put me off – I thought of throwing in a KCB vs Equity Group comparator and let the reader see what sense they would make of it. Key point to note is that the lines of the banks’ financials I have chosen to include in the analysis say something about the bank’s business. For a different sector, its own peculiarities would create interest in a different set of indicators. So here we go.

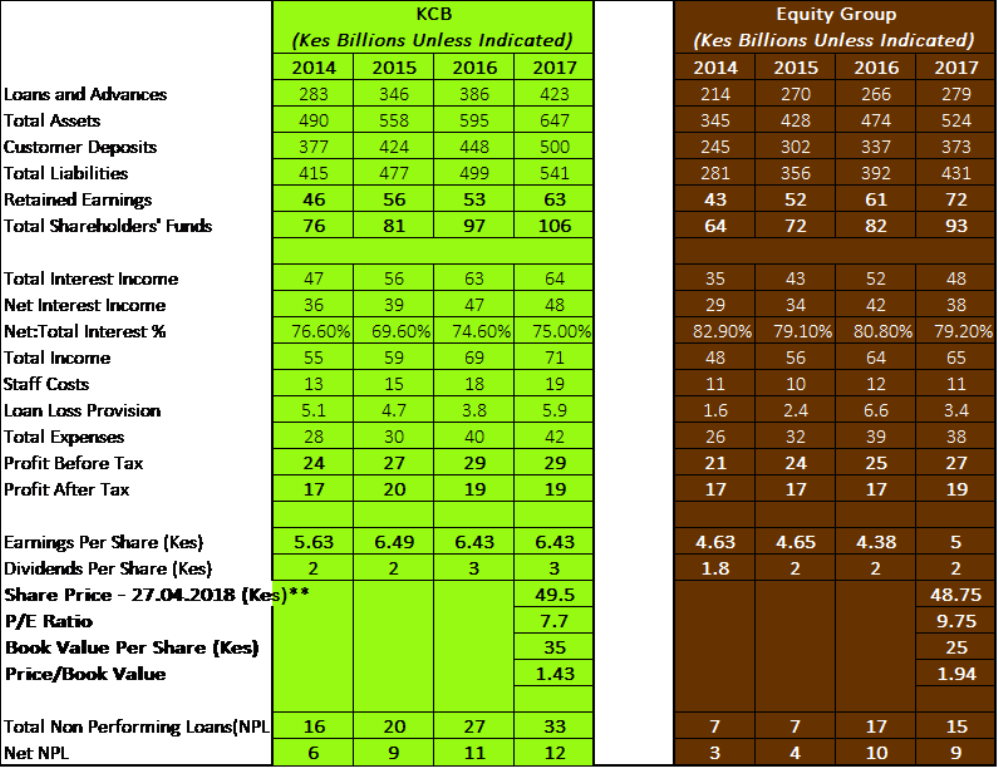

The bigger picture first. These are both impressively consistent growth businesses. They display largely similar trends. Both their shares are grossly undervalued for such a consistently profitable sector. Their PE ratios are below 10 while the entire NSE has an average PE of 14 – meaning other obviously less attractive counters are trading at PEs way above the average. To understand the implications of low PE ratios, if these two counters were to be trading at the market average of 14, KCB’s price would be 90 and Equity’s would be 70! That is what constitutes an undervaluation from an analyst’s standpoint.

On the details, based on the valuations, KCB appears a better buy than Equity Group. It boasts better PE and Price to Book Value ratios. But then its operational efficiency seems to trail Equity Group’s. For example, with total income of 71b against Equity’s 65b in 2017, KCB returned a profit after tax of 19b, similar to Equity’s. What is the implication of this into the future? Could Equity have a higher rate of earnings growth, ultimately resulting in better fundamentals than KCB?

This is not all there is to analysis.

Loads of other information is often contained in investor briefings and detailed financial statements that one should use in order to take a view on future prospects. As an example of these, KCB reported that in 2017, 87% of their transactions happened outside the branches (mobile, ATM, POS and agents), up from 77% the previous year. Equity recorded 94% of their transactions outside the branches in 2017. KCB also spent Kes 2b to release 316 members of staff – victims of a future of more technology in banking. Equity Group’s Eazzy Banking platform recorded 94.2 million transactions worth 77.8 billion in 2017 compared to 4.4 million worth 3.3 billion in 2016. This is in addition 251.6 million transactions worth 480.3 billion on the Equitel platform. With this kind of information, you have some comfort of sorts as you wire your next order funds to the broker. So as I say to the regularly investing gang on my twitter shout outs, #TwendeKazi.

4 Comments