Safaricom FY2018 Results Discussion, And What Its Future Could Look Like

2017 was not the easiest of years for Safaricom. First, the company got caught in the middle in a post-election political fight which saw a section of the opposition ask their supporters to boycott the company. There was no way whether the supporters did boycott and the effect of this on the company financially, but this was a position no business would want to find itself in.

Secondly, their CEO Bob Collymore was taken ill and had to take an extended break from the business. Finally, there has been some revival for their competitors, with Telkom being acquired by Helios, which has seen it embark on aggressive marketing and product renewal. All this was happening in a year when economic growth slowed down, hurting the profitability of most businesses in the country. In spite of these challenges though, Safaricom reported yet another year of strong growth, which is a sign of maturity within the business, and also a strong endorsement by their customers.

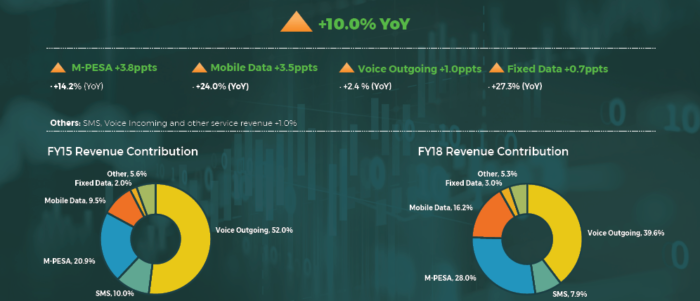

All their revenue lines had a strong showing, with the exception of voice and SMS which grew at a modest 2.4% reflective of the global trend which has seen consumers move away from conventional calling and SMS platforms, in favour of web-messaging platforms such as Telegram and Whatsapp.

It’s important to note the growth of data and M Pesa’s contribution to revenues

The Company has also retained most of this growth and its cash artillery keeps growing. As at the end of the year, it had free cashflows of KES 55.39 bn, a 27% growth from the 2012 financial year. The

What does this growth mean for Safaricom and its investors?

There is a popular saying in finance, that “trees do not grow to the sky”. Analysis on Safaricom before the release of these results seemed to share in this tone – that Safaricom was approaching the crest of its growth, and that its current share price had factored in most of the future growth (the company is trading at a high PE ratio of 21, against an average of about 14-16). However, shareholder enthusiasm in the market notwithstanding, I think Safaricom has even better days coming, especially if it is able to transform itself from a traditional telecommunications company, into financial services and tech company – which it has started to do.

Data is the next frontier

In 2000, there were about 200,000 internet users in Kenya. Today, it is a bit difficult to tell how many internet users there are in Kenya, but an estimated 26% of the population has access to the internet, a majority of whom use mobile internet. It is therefore not surprising that Safaricom’s data revenue has been on a steep upward trend.

What is next in data?

- Fibre access for more: Outside of Nairobi, there is really scanty access to fibre internet, especially for small business and home users, and yet we have seen that when you give people access to internet, they will pay for it, and they will use it.

- Investing in 5G. This will allow more users to access fibre speeds without a modem. An easier way to roll out high-speed access across the country compared to fibre which is limited to urban areas.

- Lower prices: Our data prices are lower than South Africa’s (with faster internet), but there is room to even go lower and take advantage of economies of scale. In FY2018, Safaricom lowered data prices by 29% and the resulting increased usage saw data revenue grow. This pattern is not unique – when you give people cheap internet, they use more of it.

Safaricom is well placed to fully tap into this frontier. As far as I know, it is the only Internet Service Provider with a balance sheet this strong, and also access to all market segments (business, home, and mobile internet services).

Why isn’t M-Pesa a bank already?

M-Pesa is undoubtedly entrenched as the mobile money service of choice, for almost every Kenyan. As at the end of March 2018, the service had a 20.5 million 30 day active subscribers. There is still room to achieve further ubiquity as a complete financial services solution. A few ideas come to mind here:

- Lipa Na M-Pesa, the mobile Point of Sale system has a lot of room for improvement. In addition to a better customer experience, the service can integrate better with SMEs to enable ERP integration, stocks tracking and reordering, and also purchase analytics.

- More innovation in financial services – longer-term borrowing via M-Shwari, P2P lending, investments, insurance, products for group saving and group lending etc. There is room to really diversify what M-Pesa can do, especially through the MySafaricom App.

Transforming into a digital and technology services

I see this as being two-pronged:

- Use of data and business analytics to analyze consumer patterns, which enables them further customize product offerings, and directly market these products to the consumer. For example, a customer who only watches videos on Friday evenings could receive customized offers to buy a cheaper bundle for Fridays only.

- The opportunity to play around with innovative ideas to come up with related, complementary startup businesses, or to partner with technology partners who have great ideas, and using the Safaricom reach and customer base, get these ideas to market. An example of this is Little, a cab-hailing company, that was the brainchild of Kamal Buddhabatti of Craft Silicon, backed by Safaricom. Another example is its foray into e-commerce with Masoko.

In conclusion, Safaricom has seen great (yet challenging days), but there is a possibility that the best is yet to come. What will truly define the company will be its ability to manage its mature business (telecommunications) well, while at the same time encouraging innovation and remaining fresh with the new ideas.