A Simple Guide To Investing In Treasury Bills In Kenya

Treasury bonds and treasury bills (which I will refer to as treasury instruments in the next two posts) are a way for governments to raise money from the members of the public. A good way to think about this is to imagine that the money we save collectively makes up a bank, and the government borrows from that bank, and in exchange it gives you a note against which it pays you interest for a period, and when the term of the loan is over, it pays you back your money. Because treasury instruments are considered a very safe way to invest your money, their rates of return are typically lower than other options in the market. In addition to this, the shorter the term of the investment, the lower the rate of return.

This first post concentrates on treasury bills, which are short-term investment offerings, also known as T-bills. In Kenya, you can buy three types of treasury bills: 91-day, 182-day and 364-day treasury bills, which are auctioned on a weekly basis by the Central Bank of Kenya (CBK). The minimum amount you need to buy treasury bills is KES 100,000 and incremental investments of a minimum of KES 50,000.

Before getting to the process, a few key definitions:

Face value – This is the amount the bill (think about it as a loan) is worth. For example, if you want to buy T-bills worth KES 100,000, that amount is the face value. It does not mean that you will pay KES 100,000 though, it is just a little bit more complicated than this. See the next definition.

Discount – Instead of investing your 100,000 shillings and getting X% in interest, treasury bills are sold at a discount of the face value, then you get the full face value of your investment at the end of the period. E.g if the discount for a 91-day T-bill is 7%, it means you pay KES 93,000 when you invest, then after 91 days you receive KES 100,000.

Maturity – This is the period between when you invest, and when you get your money back. As highlighted above, treasury bills issued by the government of Kenya have a 91-day, 182-day, and 364-day maturity period. Usually, the longer the maturity period, the higher the discount, though this also depends on the demand and supply of money during the issue.

Treasury bills are short term in nature, and therefore are best suited as a tool to accumulate investment capital, and also a way to “pack away” money you will not need for a period, and avoid the temptation of spending it all.

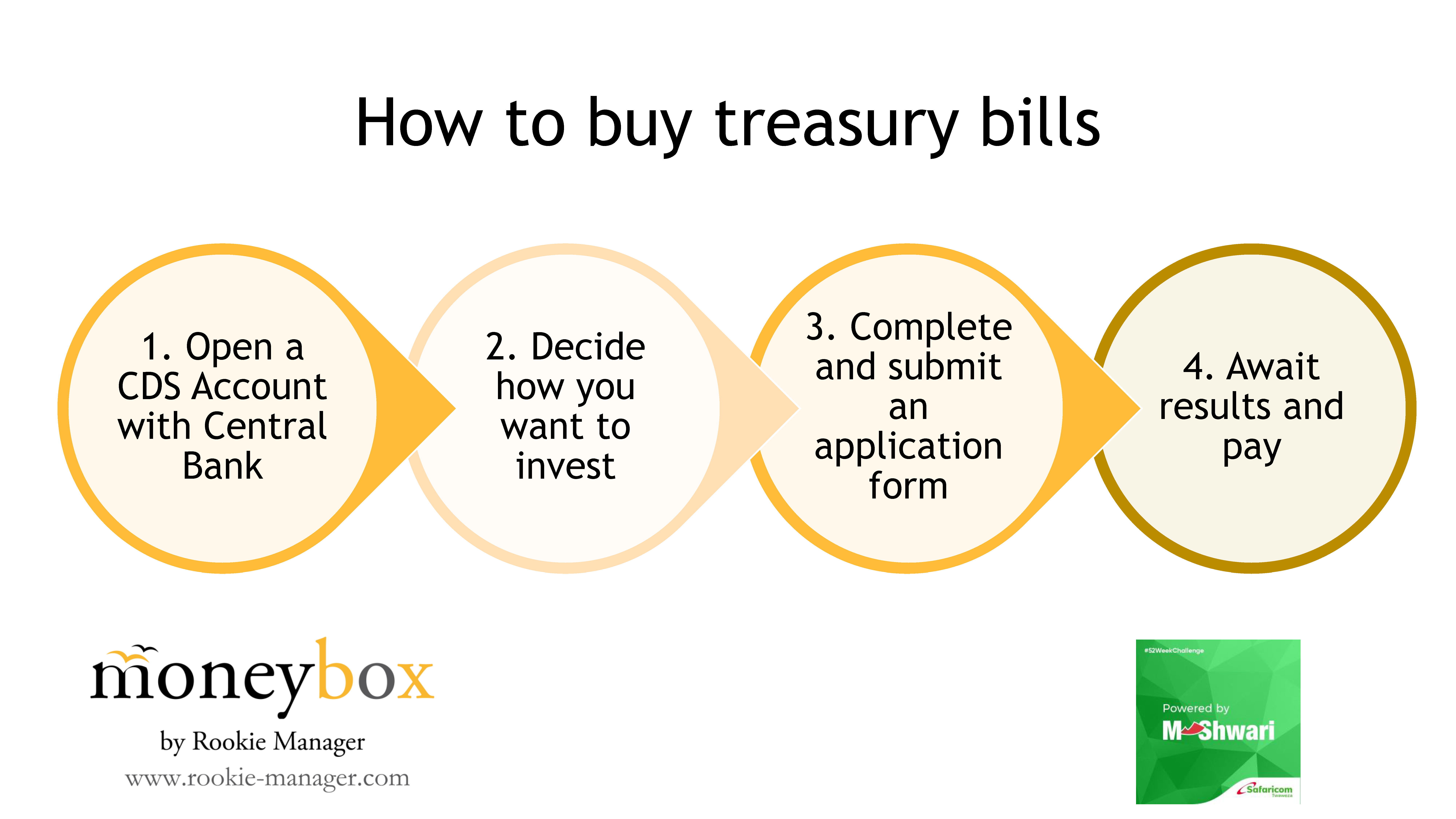

How to invest in treasury bills:

Treasury bills are sold by the Central Bank, and you can choose to buy them directly from CBK, or go through an agent – most banks and fund managers are agents. If you choose to go through an agent, they will charge you a fee for the service (a percentage of your investment), and they often have a minimum amount you can invest through them. I, therefore, would not advise a beginner to use an intermediary because of this.

The process of buying T-bills can feel daunting at first, but with time you get used to how the system works. There is an incredibly analogue first step, but once you are past that it gets easier. I am hoping CBK will extend the M-Akiba portal to T-Bills too.

1. Open a CDS account. This is different from the CDSC account we use to buy and sell shares at the stock market. To do this, you need to collect a mandate card from CBK branches in Nairobi, Mombasa, Kisumu, Eldoret or the Currency Centres in Meru, Nakuru and Nyeri. When filling it in, you must be careful to adhere to the CBK guidelines otherwise it will be invalidated:

- Individuals may hold a single or joint CDS account but NO minor accounts.

- Each individual CDS account holder/applicant MUST complete the CDS accounts specimen signature mandate card (the card)

- The card(s) should be completed in BLOCK LETTERS, neatly and clearly.

- Names MUST be written in the order that they appear on the identification document.

- NO alternations/errors.

- The card MUST not be folded or disfigured in any way.

- Signatories to the CDS account will be required to sign the card in the presence of a designated CBK Officer or any Authorised Agent.

The filled mandate card together with the following documents must then be physically submitted to the CBK:

- One recent coloured passport size photograph of the account holder. The back of the photograph MUST be certified by the applicants Bankers and stamped. It must not be stapled or glued to the card.

- The original and clear copy of the National Identity Card/valid passport/alien certificate for verification. (Note that the copies will be retained by CBK.)

- Two signatories of your Bankers, whether a commercial bank or financial institution must sign and stamp the card on the space provided, confirming the bank account details

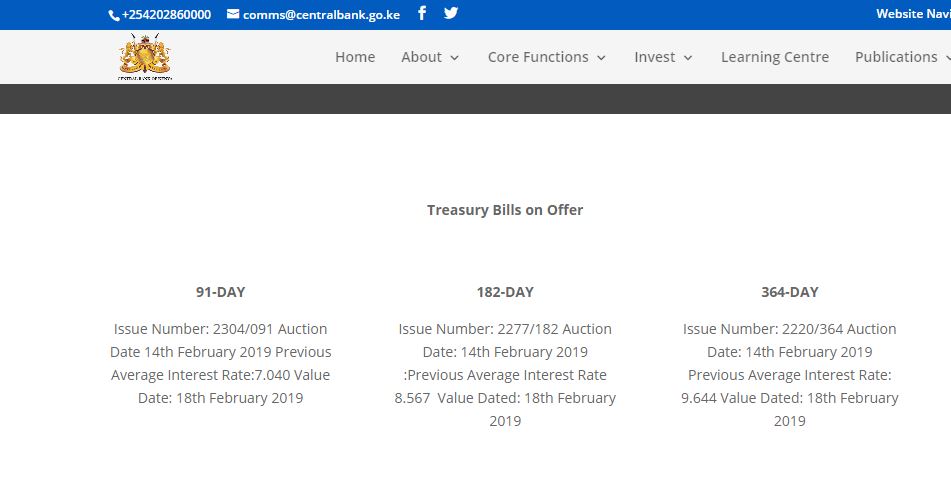

2. Decide how you want to invest. Check the Treasury Bills on offer and make a selection based on your investment period. Looking at the previous auction results gives you a good guide on the kind of returns to expect. For example, this is the page as at 8th of February.

In the previous auction, you can see that the return rates varied between 7.040% and 9.644% depending on the investment period. The site has a whole listing of the upcoming offers, and results of the previous offers in more detail.

3. Make an application to invest. This entails completing a Treasury Bill application form. Please indicate the following on the form:

- Information about the T-Bill you want to purchase. The Issue Number comes in handy here, the maturity period, and the face value you want to receive upon maturity.

- Information about yourself such as your name, phone number, CDS account number and the source of the funds.

- The form gives you the option of choosing the discount rate or return rate. Here, you can select the Competitive Range where you indicate the return rate you would like and CBK then decides what bids it will accept and not. If your rate is higher than the cutoff rate, the offer will be rejected. As a beginner, I would advise you to go for the Non-Competitive option, where your interest rate is a weighted average of the accepted bids from the Competitive investors if you are a first-time investor.

- The final section is for Rollover Instructions. To easily facilitate re-investment, investors with maturing bills and bonds can use their returns to purchase further government securities.

You must submit your application form to the Central Bank’s head office or one of its branches by 2pm on Thursday for 364, 182, and 91-day bills.

4. Get the auction results: The Central Bank’s Auction Management Committee (AMC) meets at 4pm on auction days, and after considering all received bids, determines the cut-off rate and the successful weighted average of the accepted bids. The results from the auction are published, both in a daily newspaper and on the CBK’s statistics section. If you had submitted a bid, keep an eye out on the results as you will need to make that payment by 2pm on the following Monday or, if the Monday is a public holiday, the following Tuesday.

5. Making the payment: The payment period for an auction typically closes on the following Monday at 2pm. Payments are made to the Central Bank, through cash or banker’s cheques for amounts under Kshs. 1 million or through a bank transfer for larger amounts.Successful applicants who fail to submit payments within the payment period can be barred from future investment in government securities.

6. Receiving your proceeds: At the end of the 91-, 182- or 364-day period, the face value amount of the T-Bill you bought will be credited to the bank account linked to your CDS account. Alternatively, you may choose to rollover your investment into a new forthcoming issue and in this case, you have to complete application form giving rollover instructions and submit to Central Bank before closure of the period of sale for that bill.

In the next post, we look at how to invest in Treasury Bonds.